Quick Read

This whitepaper argues that organisations typically draft sustainability reports in spring based on the prior year's template, then scramble to find supporting evidence in autumn—a sequence that fails ISSA 5000 assurance requirements because critical artefacts like materiality determinations must be created during the reporting year, not after it ends. The paper identifies two foundational decisions that determine the entire reporting workflow and proposes an alternative sequence that produces evidence-first documentation rather than justification-after-publication. By reordering the reporting year to establish materiality, data governance, and audit trails before the report is drafted, organisations can satisfy practitioner requirements and create records of what actually occurred rather than post-hoc narratives.

IN BRIEF

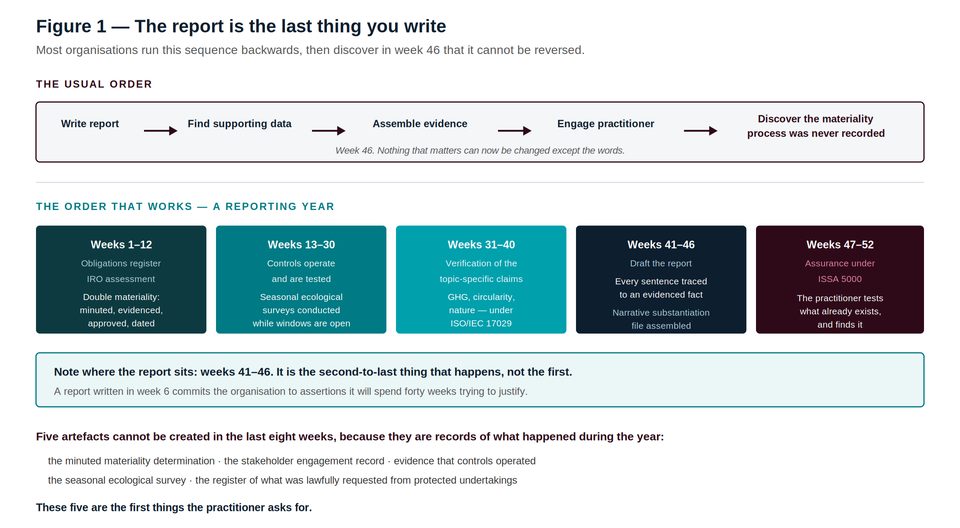

Five artefacts cannot be created retrospectively: the minuted double materiality determination, the stakeholder engagement record, evidence that controls operated during the period, seasonal ecological survey data, and the register of what was lawfully requested from protected undertakings.

Under ISSA 5000, the practitioner must evaluate the entity's materiality process where the applicable framework requires double materiality, including whether significant matters were overlooked.

Drafting the report early commits the organisation to assertions it must then spend the year attempting to justify, rather than deriving the report from evidence the year produced.

Narrative assertions of progress, leadership and improvement are within assurance scope and are the assertions most likely to attract enforcement.

A correctly sequenced reporting year places the drafting of the report in the final quarter, after the evidence exists, and before assurance begins.

Executive summary

There is a document, produced every year by every large company, whose first draft precedes its evidence. The sustainability report is written in the spring, from the previous year's report, with the numbers left blank. The blanks are filled in the autumn. In the eight weeks before publication, somebody is asked to find support for the assertions the draft has been making since March.

Nobody designed this. It is what happens when a document has a publication date and its underlying evidence has no owner.

THE FIVE ARTEFACTS THAT CANNOT BE MADE IN THE LAST EIGHT WEEKS

A minuted materiality determination recording what was considered and rejected, on what evidence, by whom. A stakeholder engagement record. Evidence that controls operated during the period, rather than a control matrix drafted for the engagement. Seasonal ecological survey data. A register of what was lawfully requested from protected undertakings. Each is a record of something that either happened during the year, or did not.

They are also, without exception, the first documents an ISSA 5000 practitioner asks to see. This paper sets out the reporting year in the order that produces them, and identifies the two decisions that determine everything downstream.

1. The order that fails

Figure 1 — Note where the report sits: weeks 41 to 46. Second to last, not first.

The failing sequence is not stupid. It is locally rational at every step.

A publication date is fixed, because the annual report has a publication date. Working backwards, a draft is needed by a certain week for design and legal review. Working backwards again, a draft is needed for internal comment. The only person who can produce a draft in March is the person who wrote last year's, and the only material available in March is last year's report.

So the draft is produced. It says the company is making progress. It says the supplier programme has been strengthened. It says the board reviews climate risk regularly. Nobody has yet checked whether any of these things is true of the current period, because the current period is four months old.

A report drafted in week six commits the organisation to assertions it will spend forty weeks trying to justify. Assurance is the moment somebody asks whether the justification arrived.

By week 46 the practitioner arrives and asks for the materiality determination. What exists is a slide deck from a workshop held eighteen months ago, and a list of topics. There is no record of what was considered and rejected, on what evidence, or by whom. The practitioner cannot evaluate whether significant matters were overlooked, because the entity cannot evidence what it considered.

Nothing can now be done. The materiality determination for a period that has ended cannot be performed after it has ended. The organisation discloses, or it does not, and either way the finding stands.

2. The two decisions that govern everything

Decision one: what is material, and how do we know

Where the applicable reporting framework requires double materiality — as the ESRS do — the practitioner must assess the entity's determination and consider whether significant sustainability matters have been overlooked. The determination is therefore not a scoping exercise conducted before the report. It is a disclosure subject to examination after it.

Impact materiality is the harder half. It rests on qualitative evidence and demands substantial practitioner judgement about the nature and extent of evidence required. A matter needs to be material from only one of the two perspectives to require disclosure — so a topic that is financially immaterial and impact-material must still be disclosed, and the evidence for concluding it was immaterial on both counts must exist.

WHAT THE MINUTE MUST CONTAIN

Date. Attendees, with authority to decide. The list of matters considered — including those rejected. For each, the evidence relied upon and the conclusion reached on impact materiality and on financial materiality separately. The approver. Six lines per matter. Nobody has this, and it takes a single properly run meeting to create.

Decision two: which controls will operate, and who will test them

Under ISSA 5000 the practitioner obtains an understanding of internal control relevant to the preparation of the sustainability information. In a limited assurance engagement they are not required to test its operating effectiveness. In a reasonable assurance engagement, where reliance is placed on controls, those controls are tested.

Either way, the controls must have operated during the period. A control matrix drafted in October, describing controls that were not in place in March, is visible immediately and is worse than having no matrix at all — because it is a document asserting something untrue about the reporting period.

3. The reporting year, sequenced

Period | What happens | What it produces that cannot be produced later |

|---|---|---|

Weeks 1–12 | Refresh the obligations register. Conduct the IRO assessment. Perform and minute the double materiality determination. | The minuted determination: matters considered and rejected, evidence, approver, date. The stakeholder engagement record. |

Weeks 13–30 | Controls operate and are tested. Seasonal ecological surveys are conducted while the windows are open. Value chain requests are made and recorded. | Evidence that controls operated. Ecological survey data. The protected undertaking register. |

Weeks 31–40 | Verification of the topic-specific claims: greenhouse gas inventory, circularity, nature — under ISO/IEC 17029. | Independent verification statements, obtained before the report describes the numbers they concern. |

Weeks 41–46 | Draft the report. Every sentence traced to an evidenced fact. Assemble the narrative substantiation file. | A report derived from evidence rather than justified against it. |

Weeks 47–52 | Assurance under ISSA 5000. | A conclusion reached on evidence that exists, rather than findings describing evidence that does not. |

The uncomfortable implication

In this sequence, the organisation does not know what its report will say until week 41.

It knows what it is accountable for, what it measured, what it controlled and what it verified — and the report is the description of those things.

Communications teams find this intolerable, and it is the entire difference between a report and a claim.

4. The narrative substantiation file

The numbers in a sustainability report receive attention because they are numbers. The sentences receive none, and the sentences are where enforcement concentrates.

Narrative assertions are within assurance scope. "We strengthened our supplier programme." "Our board reviews climate risk regularly." "We made significant progress on water stewardship." Each is an assertion of fact about the reporting period, published to investors and consumers, and each is capable of being false.

Assertion in the draft | What the substantiation file must contain |

|---|---|

"We reduced emissions by 30%" | The inventory for both periods, the boundary for each, and an analysis showing whether the reduction arose from operational change, divestment, or a change in estimation methodology |

"Our board reviews climate risk quarterly" | Four sets of board or committee minutes recording a climate risk discussion in the period |

"We strengthened our supplier programme" | The programme before, the programme after, the date of the change, and the decision that authorised it |

"We are a leader in circularity" | A stated basis of comparison, an identical functional unit, and evidence for both sides of the comparison. Most such claims are withdrawn at this point. |

"Our grievance mechanism is available to value chain workers" | The mechanism, its accessibility in the relevant languages and jurisdictions, and a case log with dates and outcomes |

THE RULE FOR THE FILE

One row per narrative assertion. Where the evidence column cannot be completed, the sentence is deleted. Not softened, not qualified with "we believe" — deleted. A sentence that requires a hedge to survive substantiation is a sentence the organisation cannot support.

5. What happens when the sequence is right

The assurance engagement changes character. The practitioner arrives in week 47 to a materiality determination that is minuted, a control environment that operated and was tested, verification statements over the material quantities, and a narrative substantiation file. Their work is to test what exists.

The engagement is shorter. Most of the practitioner's time in a badly sequenced engagement is spent establishing that evidence does not exist, and then documenting its absence.

The findings are about the subject matter rather than about the process. "The estimation method for category 3 changed without disclosure" is a useful finding. "No record exists of the materiality determination" is not a finding about sustainability at all. It is a finding about governance.

The report says less and means more. Assertions that could not be substantiated were removed in week 44, by the organisation, quietly. This is the correct place for them to be removed.

Reasonable assurance becomes available on selected metrics. Not because the organisation is braver, but because controls that operated and were tested are the precondition for it.

A well-sequenced reporting year does not produce a better report. It produces a report the organisation can defend, which is a different and rarer thing.

6. Where Speeki Guardian® fits

Speeki Guardian® is sustainability assurance under ISSA 5000, performed by Speeki as an accredited body. Speeki does not provide consulting services; details of its accreditations and their scope are published at speeki.com.

The relevance of that separation to this paper is a matter of sequence rather than ethics. A provider that helped conduct the materiality determination in week 4 cannot evaluate in week 47 whether that determination overlooked a significant matter. The engagement in week 47 is the examination of decisions made in week 4, and the examiner cannot have made them.

Guardian arrives last, deliberately. Everything that determines its outcome happened while it was not in the room.

Questions this paper answers

What cannot be created in the weeks before a sustainability report is published?

Five artefacts, because each is a record of something that either happened during the reporting period or did not. The minuted double materiality determination recording matters considered and rejected, the evidence for each, and the approver. The stakeholder engagement record. Evidence that internal controls operated during the period. Seasonal ecological survey data. And the register of what was lawfully requested from protected undertakings under the value chain cap. These are also the first documents an ISSA 5000 practitioner asks for.

Why is drafting the sustainability report early a problem?

Because it commits the organisation to assertions before the evidence for them exists. A draft written in week six says the company made progress, strengthened its supplier programme and reviewed climate risk regularly. The remaining forty weeks are then spent assembling justification for statements already made, rather than deriving the report from what the year actually produced. Assurance is the moment somebody asks whether the justification arrived.

When should the double materiality determination be performed?

In the first quarter of the reporting period, minuted and dated, recording the matters considered, the matters rejected, the evidence relied upon for each, the separate conclusions on impact materiality and financial materiality, and the approver. Under ISSA 5000 the practitioner must assess the entity's determination and consider whether significant matters were overlooked. A determination for a period that has ended cannot be performed after it has ended.

What is a narrative substantiation file?

One row for every assertion of progress, leadership or improvement in the draft report, with the evidence supporting it. Narrative assertions are within assurance scope and are the assertions most likely to attract enforcement. Where the evidence column cannot be completed, the sentence is deleted rather than softened — a sentence requiring a hedge to survive substantiation is a sentence the organisation cannot support.

When should the sustainability report actually be drafted?

In the final quarter of the reporting year, after the materiality determination, the controls testing, the seasonal surveys and the topic-specific verifications have produced their evidence, and before the assurance engagement begins. In this sequence the organisation does not know precisely what its report will say until late in the year. It knows what it is accountable for, what it measured, what it controlled and what it verified — and the report is the description of those things.

What is wrong with a control matrix drafted for the assurance engagement?

It describes controls that were not in place during the reporting period. It is visible immediately to the practitioner and it is worse than having no matrix, because it is a document asserting something untrue about the period. Controls must have operated during the period; in a limited engagement the practitioner obtains an understanding of them without being required to test their operating effectiveness, which means an inaccurate matrix may go untested while remaining on the record.

Does a correct sequence produce a better report?

It produces a report the organisation can defend, which is different. The engagement is shorter, because most of a practitioner's time in a badly sequenced engagement is spent establishing that evidence does not exist. The findings concern the subject matter rather than the absence of process. Unsupportable assertions were removed by the organisation, quietly, before publication. And reasonable assurance becomes available on selected metrics, because controls that operated and were tested are its precondition.

References and sources

IAASB, ISSA 5000, General Requirements for Sustainability Assurance Engagements, issued November 2024; effective for periods beginning on or after 15 December 2026. Requires the practitioner to assess the entity's double materiality determination where the applicable framework requires it, and to consider whether significant sustainability matters have been overlooked.

IESBA, International Ethics Standards for Sustainability Assurance (including International Independence Standards), issued January 2025; generally effective from 15 December 2026.

Directive (EU) 2026/470 (the Omnibus I directive), in force 18 March 2026 — introducing the value chain cap for protected undertakings and reducing prescribed ESRS datapoints, increasing the weight placed on materiality judgement and documentation.

Directive (EU) 2024/825, Empowering Consumers for the Green Transition, applicable from 27 September 2026 — prohibiting generic environmental claims that cannot be demonstrated.

European Sustainability Reporting Standards (ESRS), as amended, requiring double materiality.

Speeki, What ESG Report Assurance Actually Requires (Series 2, Paper 07) and The System Beneath the Opinion (Series 3, Paper 12), July 2026.

About Speeki

Speeki is an accredited ESG assurance and certification body operating in more than 100 countries. Speeki provides management system certification, verification and validation, and sustainability assurance. Speeki does not provide consulting services. Its independence is structural.

For current details of Speeki's accreditations and their scope, please refer to speeki.com.

© 2026 Speeki. This paper is provided for general information and does not constitute legal, accounting or assurance advice.